GROSS MARGIN

Financial statement is documents that provide information about the financial

situation of a company that describes the investment activities, financing, and

operations company. Financial statement such as :

— Balance sheet. Shows the entity's assets, liabilities, and stockholders' equity as of the

report date.

— Income statement. Shows the results of the entity's operations and

financial activities for the reporting period.

What

is Gross Margin?

Gross

Margin is a revenue analysis to calculate the total revenue generated from the

production number and making adjustments to the price of each unit produced

minus cost of good sold.

GM = Total Revenue - COGS

What

is the Purpose of Gross Margins?

The purpose of margins is "to determine the value

of incremental sales, and to guide pricing and promotion decision.

"Margin on sales represents a key factor behind

many of the most fundamental business considerations, including budgets and

forecasts. All managers should, and generally do, know their approximate

business margins. Managers differ widely, however, in the assumptions they use

in calculating margins and in the ways they analyze and communicate these

important figures."

How

to get Gross Margin Percentage?

Gross margin can be expressed as a percentage or in

total financial terms. If the latter, it can be reported on a per-unit basis or

on a per-period basis for a company.

"Margin (on sales) is the difference

between selling price and cost. This difference is typically expressed either

as a percentage of selling price or on a per-unit basis. Managers need to know

margins for almost all marketing decisions. Margins represent a key factor in

pricing, return on marketing spending, earnings forecasts, and analyses of

customer profitability." In a survey of nearly 200 senior marketing

managers, 78 percent responded that they found the "margin %"

metric very useful while 65 percent found "unit margin" very useful.

"A fundamental variation in the way people talk about margins lies in the

difference between percentage margins and unit margins on sales. The difference

is easy to reconcile, and managers should be able to switch back and forth

between the two. As the ratio of gross profit to cost of goods sold, usually in

the form of a percentage:

Cost of sales (also known as cost of goods sold or

COGS) includes variable costs and fixed costs directly linked to the sale, such

as material costs, labor, supplier profit, shipping-in costs (cost of getting

the product to the point of sale, as opposed to shipping-out costs which are

not included in COGS), etc. It does not include indirect fixed costs like

office expenses, rent, administrative costs, etc.

Higher gross margins for a manufacturer reflect

greater efficiency in turning raw materials into income. For a retailer it will

be their markup over wholesale. Larger gross margins are generally considered

ideal for most companies, with the exception of discount retailers who instead

rely on operational efficiency and strategic financing to remain competitive

with lower margins.

Two related metrics are unit margin and margin

percent:

Unit margin

($) = Selling price per unit ($) – Cost per unit ($)

Margin (%) = Unit

margin ($) / Selling price per unit ($)

"Percentage margins can also be calculated using

total sales revenue and total costs. When working with either percentage or

unit margins, marketers can perform a simple check by verifying that the

individual parts sum to the total."[1]

To verify a

unit margin ($): Selling price per unit = Unit margin + Cost per Unit

To verify a

margin (%): Cost as % of sales = 100% – Margin %

"When considering multiple products with

different revenues and costs, we can calculate overall margin (%) on either of

two bases: Total revenue and total costs for all products, or the

dollar-weighted average of the percentage margins of the different

products."[1]

How gross margin is used in sales?

Retailers can measure their profit by using two basic

methods, markup and margin, both of which give a description of the gross

profit. The markup expresses profit as a percentage of the retailer's cost for

the product. The margin expresses profit as a percentage of the retailer's

sales price for the product. These two methods give different percentages as

results, but both percentages are valid descriptions of the retailer's profit.

It is important to specify which method you are using when you refer to a

retailer's profit as a percentage.

Some retailers use margins because you can easily

calculate profits from a sales total. If your margin is 30%, then 30% of your

sales total is profit. If your markup is 30%, the percentage of your daily

sales that are profit will not be the same percentage.

Some retailers use markups because it is easier to

calculate a sales price from a cost using markups. If your markup is 40%, then

your sales price will be 40% above the item cost. If your margin is 40%, your

sales price will not be equal to 40% over cost (in fact, it will be

approximately 67% above the item cost).

Markup

The equation for calculating the monetary value of

gross margin is: gross margin = sales – cost of goods sold

A simple way to keep markup and gross margin factors

straight is to remember that:

- Percent of markup is 100 times the price difference divided by the cost.

- Percent of gross margin is 100 times the price difference divided by the selling price.

Gross margin (as a percentage of Revenue)

Most people find it easier to work with gross margin

because it directly tells you how much of the sales revenue, or price, is

profit. In reference to the two examples above:

The $200 price that includes a 100% markup represents

a 50% gross margin. Gross margin is just the percentage of the selling price

that is profit. In this case 50% of the price is profit, or $100.

In the more complex example of selling price $339, a

mark up of 66% represents approximately a 40% gross margin. This means that 40%

of the $339 is profit. Again, gross margin is just the direct percentage of

profit in the sale price.

In accounting, the gross margin refers to sales minus

cost of goods sold. It is not necessarily profit as other expenses such as

sales, administrative, and financial must be deducted. And it means companies

are reducing their cost of production or passing their cost to customers. The

higher the ratio, the better.

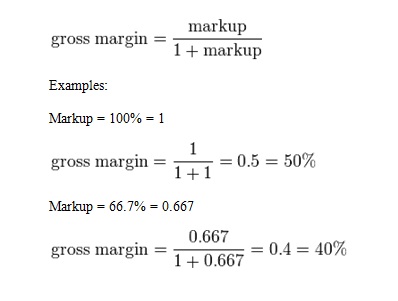

Converting between gross margin and markup (Gross Profit)

Converting markup to gross margin

Examples:

Converting gross margin to markup

Examples:

Using gross margin to calculate selling price

Given the cost of an item, one can compute the selling

price required to achieve a specific gross margin. For example, if your product

costs $100 and the required gross margin is 40%, then

Selling price = $100 / (1 – 40%) = $100 / 0,6 =

$166,67

Differences between industries

In some industries, like clothing for example, profit

margins are expected to be near the 40% mark, as the goods need to be bought

from suppliers at a certain rate before they are resold. In other industries

such as software product development the gross profit margin can be higher than

80% in many cases.

Tidak ada komentar:

Posting Komentar